Forty-eight — bye, Chinese stock market

This is my third article in the "Goodbye" series, following the previous two about ACM and Baidu.

This piece objectively documents my financial journey over the past few years, along with some personal reflections.

Here, "red" represents gains, and "green" represents losses.

The content of this article does not constitute any investment advice and represents only personal opinions. The stock market involves risks; invest with caution.

Main Text

The Tuition Fee for Entering the Market

I first got into financial management in 2021 (while preparing for the early college entrance exam during my second year of high school). At that time, our school didn't prohibit the use of mobile phones. Since I had turned 18, I was able to access the financial management section on Alipay. One of the "benefits" Alipay offered to new users was collecting "gold tickets" that could be used to purchase gold and exchange it for money. When I had collected enough gold tickets to meet the task requirement, I initially thought they could be directly withdrawn into my Alipay balance. However, it turned out that I had to purchase something to use these gold tickets. In order to use up the gold tickets I had, I spent over 200 yuan (which was most of my pocket money at the time) and went all in on something called Bosera Gold ETF Connect C (yes, back then I didn't even know this thing was called a fund).

After that, I went back to studying for my college entrance exams. I thought I had scored a freebie by taking advantage of the gold tickets, but a few days later, during a break from solving practice problems, I checked my returns—only to find that I had lost over 11 yuan! That was the cost of a whole lunch for me. I thought to myself, I couldn't let the losses continue like this—what if I lost even more later? So, like a startled bird, I sold that one gram of gold. As a result, my loss expanded from over 11 yuan to 13.12 yuan! I was extremely frustrated at the time. I had paid a "painful" price for trying to take advantage of a few hundred gold tickets.

After calming down, I looked up information online and learned some basics about funds:

- Unlike bank deposits, funds fluctuate in value. Some funds are based on currencies and bonds, offering lower returns but also lower risks; others are based on stocks and commodities, offering higher returns and higher risks (and I realized that what I had bought fell into the latter category).

- ETF stands for Exchange-Traded Fund, meaning the fund's value is tied to a certain index (in this case, the price of gold). Even though my financial knowledge was limited back then, I knew that gold prices change (otherwise, why would gold stores display "Today's Gold Price: xxx.xx"?). This helped me understand why I had inexplicably lost 12 yuan.

- The purchase fee for funds is relatively low (around 0.15%), but the redemption fee is higher if you sell too soon (about 1.5% within the first seven days, decreasing afterward). That's when I realized the extra yuan I lost was actually the redemption fee. Ouch.

After paying this 13.12 yuan "tuition fee," I officially stepped into the world of financial management.

Mother's Entry into the Market

After the college entrance exam results were released, and the young student successfully gained admission, I welcomed a leisurely summer vacation. At that time, the stock market was booming, and my mother somehow came across a course related to funds and started attending lectures. She persuaded me to invest in a few funds as well. She recommended three funds to me at the time: Penghua Liquor Index A, Qianhai Kaiyuan New Economy Flexible Allocation Mixed A, and Baoying Advantage Industry Flexible Allocation Mixed A. She advised me to stick with dollar-cost averaging and explained the concept of the "smile curve" to me. I found the theory of the smile curve quite reasonable but chose not to start investing immediately.

In addition, I occasionally observed the content of my mother's course, which seemed to involve analyzing corporate financial reports, price-to-earnings ratios, price-to-book ratios, and other such topics. Each lesson appeared to have assignments that needed to be submitted to the teaching assistant. Since I wasn't particularly interested in these topics at the time, I didn't delve deeper into them.

Of course, after Alipay noticed that I had suddenly started dollar-cost averaging into a few funds, it also recommended some other funds to me. I chose one labeled "Alipay Gold Selection" — Xingquan Business Model Preferred Mixed (LOF) — and began investing regularly. My mother took a look at the fund's composition and teased me, saying the consumer industry wasn't performing well and didn't yield high profits. I checked the performance trends over the past three years and found that its profits were indeed significantly lower than those of the three funds she had recommended (the others had returns of 200% to 300%, while this one had a meager 100%). But I thought to myself, since it was labeled "Alipay Gold Selection," there must be a good reason for it. So, I decided to continue holding it, curious to see whether my judgment would prove right or if my mother's would prevail.

The Beginning of a New Semester

The new semester brought a series of fresh experiences, one of which was activating a China Construction Bank (CCB) card linked to my student information for scholarship transfers. At the time, CCB was also promoting a co-branded credit card with Bilibili exclusively for students, so I applied for it as well. The CCB salesperson seemed to handle a lot of things for me, including but not limited to activating both my debit and credit cards, teaching me how to participate in IPO subscriptions, and even opening a securities account for me while I was half-asleep—transferring 0.01 yuan into it. It also seemed like he set himself up as my dedicated account manager (I can't quite remember the exact title).

I asked him a question about returns: Is there really no investment method that can consistently outperform inflation? He didn't answer my question directly. Instead, he said that any investment claiming returns above 6–7% annually is either unstable or a scam. Then he added that it was pretty impressive for a university student like me to already be thinking about financial management.

Later, I found out that the credit limit on that CCB card was only 0.01 yuan. Apparently, I needed to link it to a parent's bank card to lift this restriction and fully activate it. Since I had no real need for a credit card at the time and held a stereotypical fear of them, I ended up canceling it. As for IPO subscriptions, they required a principal investment of 10,000 yuan, which I found too expensive, so I never proceeded with it. The newly opened securities account was left completely unused, treated like worthless clutter.

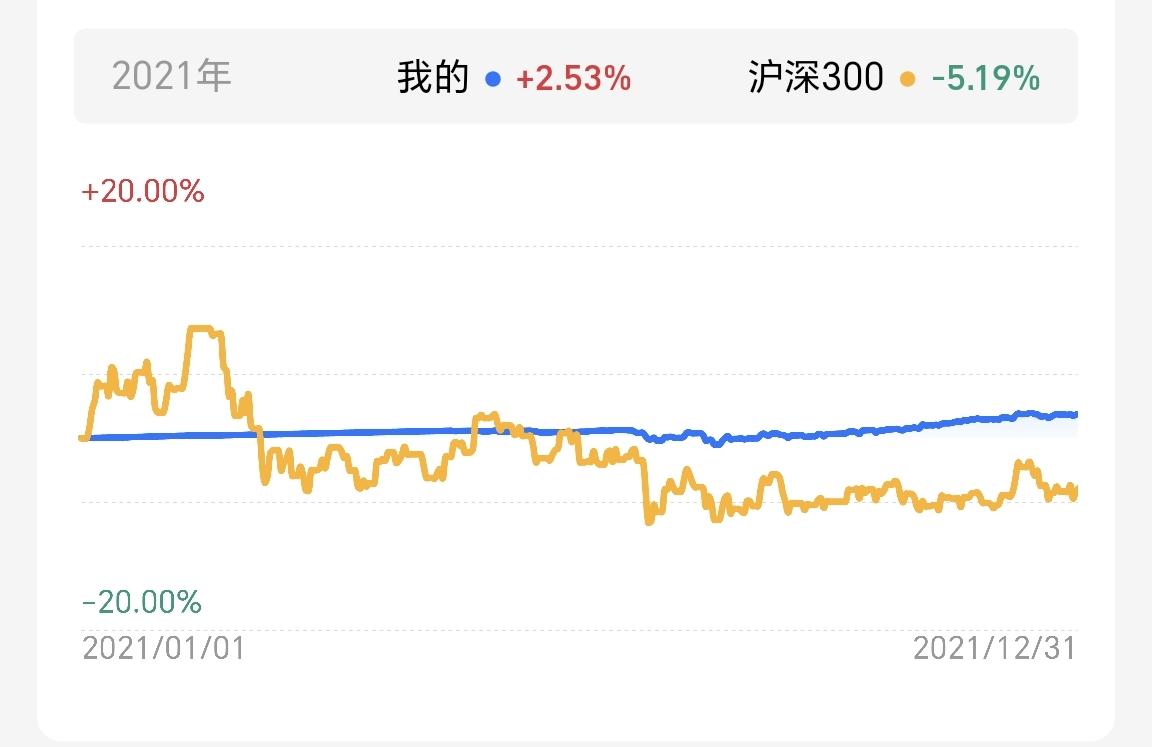

Over the next four months, I watched my balance grow steadily. By the end of 2021, my return rate was 2.53%, outperforming 90.68% of investors nationwide. The frustration I had felt earlier after losing 13.12 yuan on gold investments seemed like a distant memory. I thought to myself, “So this is what financial management is all about? It's actually quite simple.” Then I wondered, why did my high school politics teacher say she lost over 200,000 yuan in the stock market? I couldn't understand it.

A Year of Downturn

Then came 2022. In January of that year, I looked at my investment funds and saw that, except for Penghua Liquor Index A, all the others had achieved a return rate of over 10%. I wondered whether I should cash out while I was ahead. At the time, my mother thought the gains weren't substantial enough and suggested I hold on a bit longer to see if they would rise further. After some thought, her reasoning made sense, so I sold 50% of each of my funds—except Penghua Liquor Index A—and kept the remaining 50% to observe.

What happened next left me utterly stunned. From the moment I started selling, all the funds began to decline. I watched as my returns gradually dropped from double-digit positive numbers to single-digit positive numbers, then turned into single-digit negative numbers, and eventually even double-digit negative figures. To make matters worse, I continued with my regular fixed investments, which meant that even if the decline rate stayed consistent, I was losing more money each day. At that point, I didn't know whether to laugh or cry. I felt like crying because I was staring in disbelief at Penghua Liquor's over 30% loss. Yet I also felt like laughing because the timing of my sell-off had been so precise (my mother even joked that I should study finance), and the fund that lost the most happened to be the one I wasn't regularly investing in (otherwise, the losses would have been far greater).

Of course, my Xingquan funds were also in the red, but thanks to the cost-averaging effect of regular investments, the percentage loss wasn't too high (though the absolute amount was still significant). Still, I held onto the belief in the "smile curve" theory, so I didn't make any changes and continued with my fixed investments. At one point in the middle of the year, some funds briefly turned positive, but I didn't sell immediately, thinking they would bounce back to the previous 10% level. And then—they turned negative again. As a reader, you can probably imagine how I felt at that moment.

In 2022, my return rate was -1.59%, outperforming 11.63% of investors nationwide.

Credit Cards, Foreign Exchange, Virtual Currency, and Leverage

At the end of 2022, ChatGPT was taking the world by storm, and I was among the first wave of users. The following year, ChatGPT launched version 4.0, which required a monthly subscription of $19.99. By then, my financial situation was no longer as tight as it had been in high school—I could afford 140 RMB a month. The real challenge was that ChatGPT didn't support mainland China, so I couldn't use WeChat Pay or Alipay. It was incredibly frustrating to have money but no way to spend it!

So, I scoured the internet for ways to purchase ChatGPT Plus and stumbled upon the concept of virtual credit cards. That's how I learned about Visa and MasterCard. The first virtual credit card platform I came across was Depay (now renamed Dupay). It didn't support Alipay or WeChat Pay for top-ups either; the only option was to use USDT. That's when I realized that USDT, like Bitcoin (which I'd heard about in 2021 when someone was mining it live right before the Youth Proficiency Exam), is a virtual currency. These currencies aren't just obtained through mining—they can also be exchanged for fiat currency through trading platforms.

So, I spent 200 RMB to buy about $27 worth of USDT on Binance (with a small transaction fee). Then, transferring it to my Depay wallet via the BEP20 blockchain cost another $2 or so in fees. Converting USDT to USD came with an exchange rate spread (0.99) and another fee (around $1–$2). In the end, only about $23 made it to my virtual credit card. Let's just say the middlemen made quite a profit along the way.

While figuring this out, I also learned about financial strategies involving virtual currencies. The most basic approach is holding long-term (HODLing). A slightly more aggressive tactic is spot trading (similar to short-term trading in the A-share market). For those seeking even higher risks and rewards, there are futures and contracts, often combined with leverage. Online, you can find stories of people gradually achieving financial freedom using these tools and compound interest, as well as tales of those who made tens of millions through speculation only to lose it all. At the time, though, I was just focused on solving my ChatGPT problem and had no interest in the money-making potential of virtual currencies.

What is leverage? Let's take 10x leverage as an example. Suppose you have 100 RMB in capital. With 10x leverage, you "borrow" 900 RMB from the market (though, in practice, contracts are just agreements—you don't actually borrow money from someone else). If the index you're tracking (which could be a virtual currency, stock index, or something else) rises by 10%, your 1000 RMB becomes 1100 RMB. After repaying the "borrowed" 900 RMB, your initial capital effectively doubles. However, if the index drops by 10%, you lose all your capital. If you don't add more funds, you get "liquidated."

Around June 2023, I was preparing to attend a summer camp at the National University of Singapore. Since I'd grown accustomed to not using cash, I wanted to avoid paper money by getting a multi-currency credit card. For someone with no income, getting an ordinary credit card is already quite difficult, let alone a multi-currency one. But luck was on my side—I applied for a MasterCard multi-currency credit card through my bank's app and, surprisingly, got approved. I just needed to activate it in person. The bank teller was even surprised and tried to upsell me by applying for a domestic credit card, but two attempts failed. In the end, she set a monthly limit of 10,000 RMB on my multi-currency card, which I was quite happy with. (Although, once in Singapore, my card's usefulness was limited since bank cards there need to be linked to a Singaporean ID, which obviously wasn't possible for me.)

Regarding foreign exchange, I paid attention to the SGD-to-CNY exchange rate when paying my tuition fees to NUS. At the time, the rate was around 5.21. By July 2023, the SGD had strengthened significantly, reaching 5.41. I felt relieved—I'd saved myself another 1,000 RMB. Tired of the intrusive behavior of domestic smartphones, I bought a Google Pixel 7a in Singapore, which allowed for direct bootloader unlocking (and I must say, its camera is fantastic). The Google ecosystem there was so seamless that I ended up not even wanting to unlock the bootloader (quite contradictory, I know—haha).

By August, some of China's major real estate companies began facing issues, and the USD strengthened against the CNY due to interest rate hikes, with the exchange rate reaching around 7.3. Pessimistic about the domestic economic outlook and considering studying abroad, I opened a Visa dual-currency (CNY-USD) debit card with Bank of China and transferred $5,000 into its USD account twice (at rates of 7.12 and 7.28). In hindsight, this move resulted in a short-term loss, as the rate has since dropped back to 7.1, leaving me with a paper loss of about 600 RMB. But it doesn't really matter—as long as I don't convert that $5,000 back to RMB, I can tell myself I haven't lost anything, haha. It seems true what they say: trading forex is harder than trading stocks or commodities.

On a side note, around this time, the Android version of ChatGPT was released. Since Google Play's card binding requirements aren't as strict as Stripe (used by OpenAI) regarding card origin, I found a workaround: I downloaded the ChatGPT app on my Pixel phone, linked my MasterCard credit card to Google Play, and set up a monthly subscription for ChatGPT Plus. This completely eliminated the need for the time-consuming and costly virtual currency workaround, finally solving the payment issues I'd faced with domestic accounts.

Second and Third Adjustments

Getting back to the topic of funds, by mid-year, the stock market had improved somewhat, and all my returns were back in the green. But one must learn from experience, so I liquidated the underperforming Penghua Beverage Index A (cumulative return: ¥11.68) and gradually reduced my holdings in the Invesco Great Wall Preferred Business Model Mixed (LOF). I also started a fixed investment plan for the Qianhai Kaiyuan New Economy Flexible Allocation Mixed A.

As I had anticipated, after I reduced or closed my positions, the stock market began to decline again. Once more, I watched my returns shift from single-digit green figures to single-digit red figures, and then to double-digit red figures (though this time, the drop wasn't as drastic as 30%). Because I had taken profits in time, these losses were within my expectations, so I remained relatively unfazed. After that, I continued with my fixed investments and paid little attention to the stock market.

Let me briefly discuss the final outcome of the Penghua Beverage Index A fund that I liquidated. After I sold it, the fund initially rose slightly but then entered a period of volatile decline. As of the time of writing, that fund has fallen more than 20% compared to the price at which I sold it.

By the end of the year, the stock market experienced a minor rally, and my funds saw another wave of profits. Surprisingly, the biggest contributor this time was the Invesco fund, which I had previously been less optimistic about, while only the recently added Qianhai fund was in the red. Overall, however, my rate of return for 2023 reached 4.99%, outperforming 99.22% of investors nationwide.

From the end of 2023 to the beginning of 2024, I wasn't paying much attention to the performance of my funds. But as I began to feel the economic pressures—initially affecting high-level sectors like real estate—trickle down to tangible aspects of daily life, I started monitoring my investments again. Unsurprisingly, they had turned red once more! My earlier pessimism about the economy was gradually becoming a visible reality. As an urban dweller, the most glaring evidence was the unfinished buildings and the cries of frustration plastered on concrete walls. Although these outbursts were often short-lived, fading away after a few days or forgotten amidst the city's facade of prosperity, the red numbers in my account didn't lie. Because of this, holding investments long-term began to seem increasingly unrealistic, and my mindset gradually shifted from bullish (long-term optimism) to bearish (long-term pessimism).

By mid-May 2024, the stock market experienced another rally. I followed the same strategy as before: if an investment broke even, I sold half. As a result, I only sold my Invesco holdings (which had recovered), while my other funds remained unfortunately a few percentage points in the red, so I left them untouched. This rally didn't last long either, and the market soon entered another prolonged slump. Once again, I stuck to my fixed investment plan and ignored fund-related news until the end of September this year.

The Final Move

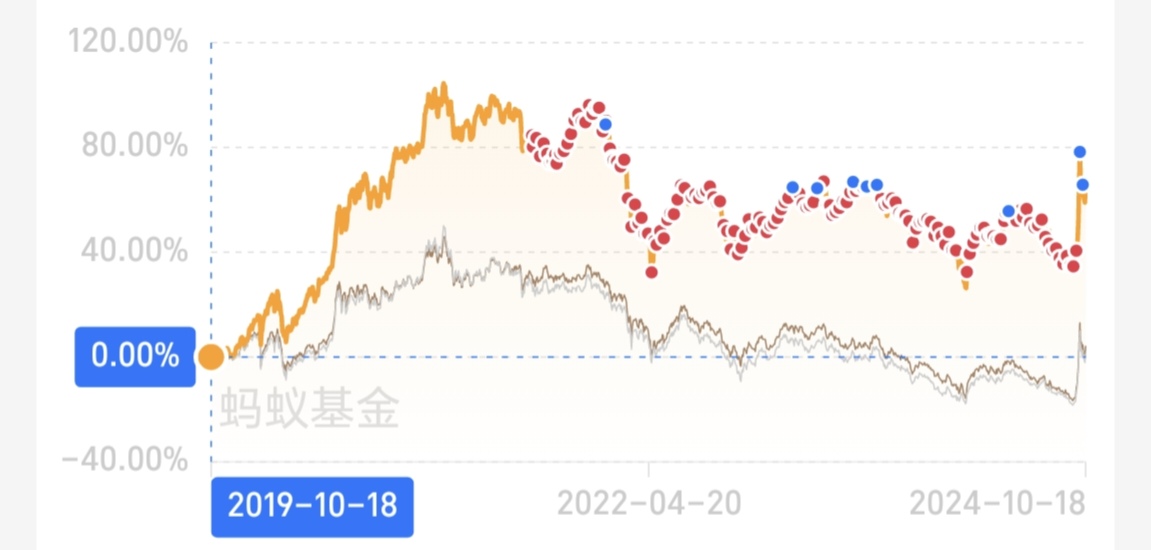

It was after securing my postgraduate recommendation, during a period of idleness, that I stumbled upon news of the stock market's "crazy bull run." I went back to Alipay to take a look at the Shanghai Composite Index's K-line chart, and my first impression was that the shape didn't look right. Moreover, all my funds had returned to the scenario from early 2022, where each was showing a profit of over 10%. Coupled with the news of crowds frantically opening brokerage accounts and even taking out loans to manually add leverage, my inner thought was: This market is simply insane, utterly irrational. But it was already past 3 PM, and if I wanted to redeem my funds, I would have to wait until October 8 to make the move. To be honest, that National Day holiday was somewhat anxiety-inducing. The stock market felt too detached from fundamentals, and I was worried that a sharp drop would hit on October 8. I told a foreign classmate I met in Singapore that I planned to sell 80% of my holdings on October 8. He said, "You've realized the casino-like nature of the Chinese stock market. You've got insight."

Finally, October 8 arrived. I was completely immersed in watching the market, even catching a few lines of that morning's press conference. As expected, the conference offered little substance. However, the market didn't experience the sharp drop I had anticipated. Instead, it opened high and closed low, rising by about 3% by around 2 PM. So, I didn't rush to sell 80% as initially planned. Instead, I stuck to my earlier strategy and sold 50% of all my funds before 3 PM, then continued to watch how the market would play out in the following days.

That evening, I looked up how previous similar bull markets had unfolded. Most opinions suggested that after a sharp initial surge, the market would oscillate at a relatively low level, shaking out bears and less determined bulls. Then, once trading volume decreased, it would enter a slow bull phase. That logic made sense. So, when the Shanghai Composite plummeted 6% the next day, I remained unfazed and continued to observe. For the rest of the week, I kept an eye on the market trends. Although the stock market was indeed oscillating, it rose less and fell more. Even though I had taken profits on half of my funds on Monday, by the end of the week, 80% of Monday's gains had been wiped out. I was reminded of the regret I felt in early 2022, watching double-digit profits gradually turn into double-digit losses. I also felt that staring at stock charts was rather meaningless—there are far more interesting things in the world than making money. So, I decided to liquidate all my holdings on a day when the market rose the following week.

Having done my homework, I knew that if the index fell sharply near the close on Friday, the probability of a rise the following Monday (October 14) would be quite high. And indeed, that's exactly what happened. The market rose by 2.07% that day. Initially, I planned to sell everything and deposit the proceeds into Yu'e Bao. But the returns on Yu'e Bao were too low, so I chose to move the redeemed funds into bonds instead, as the stock and bond markets typically move in opposite directions. Unexpectedly, my judgment proved correct once again. Over the next three days, the market continued to fall, with only a significant rally on Friday, though it still didn't reach the levels at which I had sold.

By the way, I've gradually come to realize that even among equity funds, choosing different fund managers can lead to vastly different outcomes, even if these funds generally rise and fall with the market. For example, the Xingquan Fund managed by Ms. Qiao Qian achieved a total return rate of 15.42% by the time I liquidated my position, while another heavily weighted fund, Qianhai, only managed 6.55% even with the support of this surge. As for the underperforming Penghua Alcohol fund, I don't even want to mention it. Although Ms. Qiao Qian didn't graduate from a top-tier university and holds only a standard master's degree, her professional competence is widely recognized. She has shown me that in the financial industry, standing out through professional ability isn't limited by gender. I hope to see more such examples in the future, where everyone, regardless of gender, can succeed in the workplace based on merit.

So far, my annual return rate stands at 8.96%, outperforming 99.04% of national investors. I can finally understand, from personal experience, what that China Construction Bank staff member told me: To achieve an annual return of over 6% or 7%, it's nearly impossible to just go all-in on one product and do nothing. Now that I'm out of the market, I occasionally wonder: If I had sold everything on October 8, could I have pushed my return rate to 10%? Or if I had held on a bit longer, would I have truly waited for the slow bull to arrive? Time will tell the final answer, but whatever it is, I no longer care. Because I firmly believe—

I want steady happiness, capable of withstanding the cruelty of doomsday.

—— "Steady Happiness" by Eason Chan

(End)

Appendix

Fund Performance and My Operations

Sorted by return rate from highest to lowest:

Fullgoal Business Model Preferred Mixed (LOF)

Qianhai Kaiyuan New Economy Flexible Allocation Mixed A

Baoying Advantage Industry Flexible Allocation Mixed A

Penghua Liquor Index A

Annual Return Fluctuation

2021:

2022:

2023: